University spin outs commercialise the very cutting-edge of research activity from these institutions. Given the potential economic impact these companies can have, they are of a great deal of interest to policymakers. But how many spin outs are trading today? Which institutions do they come from? And where do they operate?

This blog presents 7 facts on UK spin outs using data from The Data City’s Industry Engine. It looks at any spin out from a UK university that is trading today and was incorporated after 2011.

Fact 1: Spin outs account for a very small part of the business base, but punch above their weight

We identify around 1,540 businesses that were incorporated since 2012 and are still trading today. This is a very, very small proportion of the overall business base overall. In fairness, comparing spin outs to businesses like cafes and dry cleaners isn’t very helpful. But even focusing in on the cutting-edge part of the economy shows that they still account for a small proportion of the total – they make up just 1.6% of all ‘frontier’ businesses that we classify using our Real Time Industrial Classification (RTIC) definition.

What we don’t know is whether this is an underperformance relative to other countries. Given that the recent Hickson Review of investor-spin out links said that the UK is second only to the USA in terms of spin out creation, it might well be that we should manage our expectations on how many businesses we expect university research to create directly. The Data City will have a more detailed answer to this soon when we launch our US, French, German and Irish products.

That said, spin outs do attract a disproportionate amount of investment, which helps explain why they get policymakers excited. Likely reflecting attractive potential returns from these businesses:

- 55% of spin outs that are trading today have received at least one investment round (excluding early-stage grants from public bodies), compared to just 5% of a wider comparison group of cutting-edge companies that fall into one of The Data City’s RTICs.

- 9% have reached expansion and scale up (at least Series B), compared to 1% of the comparison group.

- 1% of spin outs have reached Post-IPO & Later Financing, compared to just 0.1% of the comparator firm base.

So investors see spin outs as a very investable part of the UK’s cutting-edge business base.

Fact 2: The US cherry picking of UK spin outs seems slightly overblown

An ongoing debate in UK economic policy is the leakage of the UK’s most innovative companies to the US in search of easier access to investment (particularly later stage investment). This applies to conversations about spin outs too, with the Hickson Review raising US buyouts as a concern.

While there certainly are examples, such as IonQ’s recent purchase of Oxford Ionic, there is no compelling evidence that this is systematically happening. Of the spin outs that are trading today, we identify 39 as being owned by a US company. This is 2.5% of all spin outs.

This data doesn’t capture companies that have been bought by US companies and absorbed into them, or those that have moved to the USA. But again, this is small. Looking at spin outs that are no longer trading in the UK, we find:

- 10 spin outs that have been bought out by US companies and have ceased trading, such as Bloomsbury AI.

- Two companies that have moved to the US: Pepgen (which works on genetic diseases) and WaveBreak (formerly Wren Therapeutics, which works on neurodegeneration).

It takes a lot of digging to find these companies, so these numbers may not be comprehensive. But if there are other examples, the number will be small.

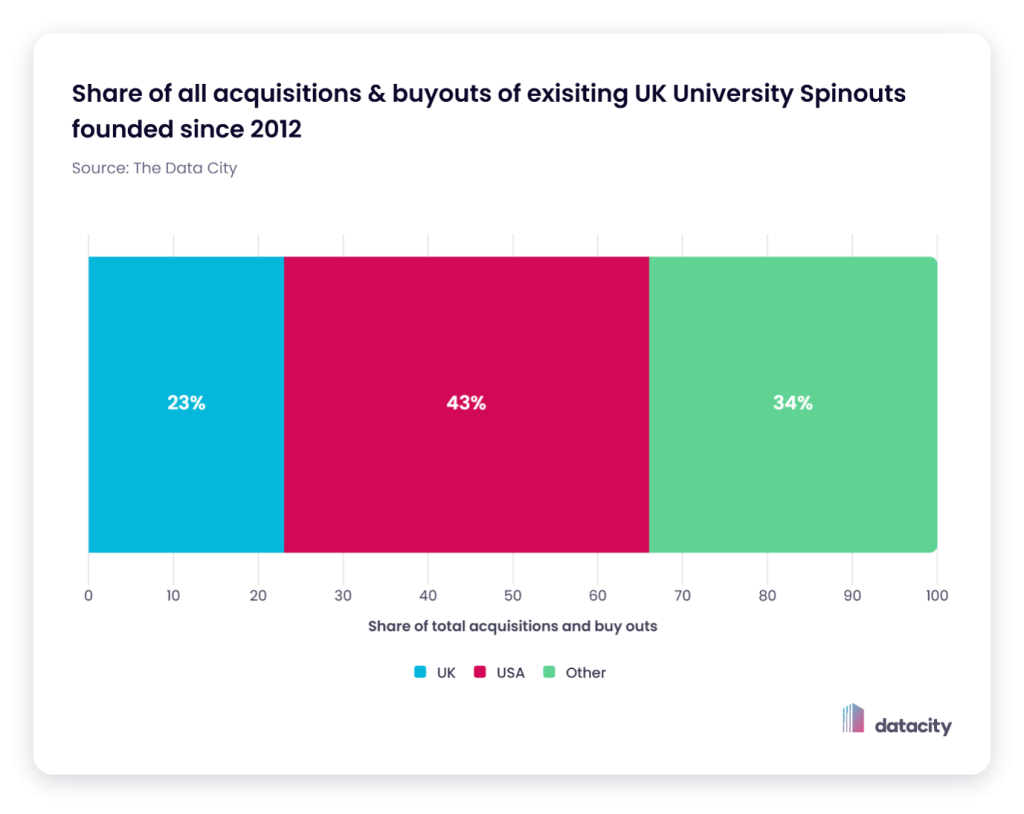

It is true is that the US dominates when it comes to acquisitions and buy outs of spin outs, with US companies more likely to do this than even UK ones (Figure 1). But in absolute terms, they are – currently at least – small numbers.

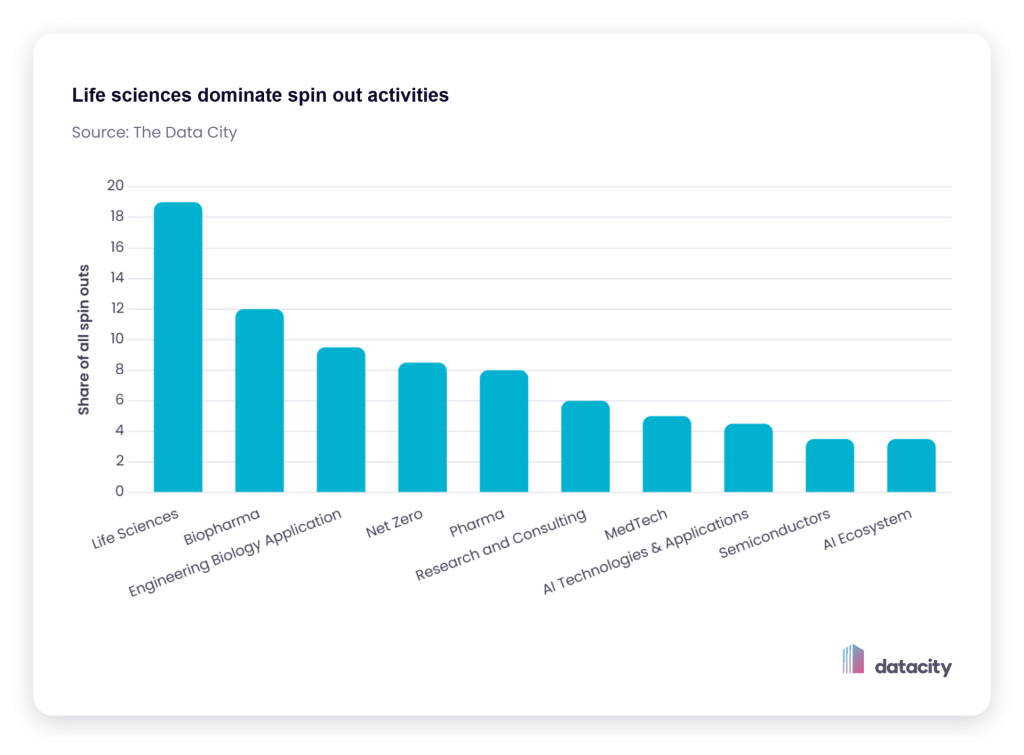

Fact 3: Spin outs are overwhelmingly in Life Science and related activities

The three most common sectors that spin outs operate in are in Life Sciences or related (see Figure 2). Around one fifth are in Life Sciences alone. And looking across a broader definition that also includes Biopharmaceutical, Pharma, OMICs, MedTech and Engineering Biology Application shows that at least 32% of spin outs – that’s almost one in three – do something that is Life Sciences related. This activity isn’t confined to a handful of universities either- it is the most common sector for half of all institutions that have an active spin out.

The Government identifies Life Sciences is one of eight priority sectors in its Industrial Strategy, and this data suggests it is this sector where UK university research has the biggest impact.

Looking at subsectors within these areas shows that it is BioTech – a sector that uses living systems, organisms, or enzymes and cells to develop products – where activity is particularly concentrated. Autolus, which spun out of UCL, is an example. One in every 8 spin outs trading today has activities in Biotech. This compares to fewer than 1 in 100 of all cutting-edge companies in the UK.

Sector underrepresentation is more difficult to identify. For example, there aren’t many FinTech companies that spin out of a university. But this is likely to be because developing ideas in FinTech doesn’t require a university research setup in the way that Life Sciences does. From an Industrial Strategy perspective, this suggests which areas spin outs may have a larger or smaller role to play. One area that may be underrepresented though is Advanced Manufacturing. While the sector accounts for 6% of all cutting-edge businesses, it accounts for 2% of spin outs. Given the R&D intensive nature of this sector, it raises questions as to whether we should see more of this activity coming out of academia.

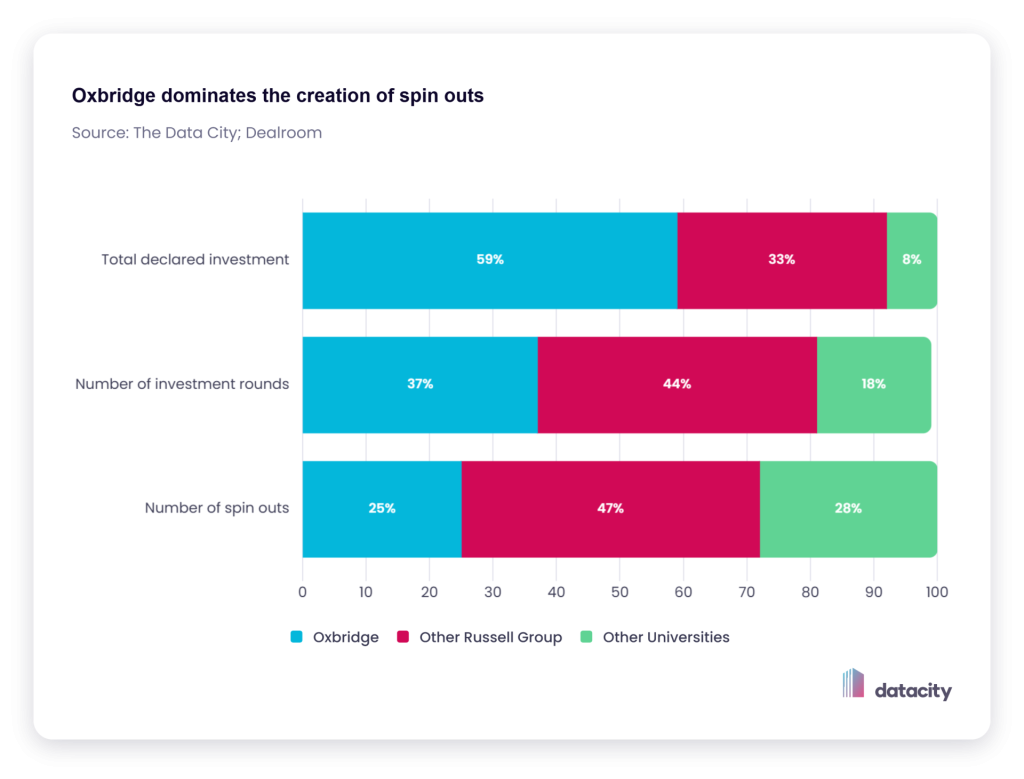

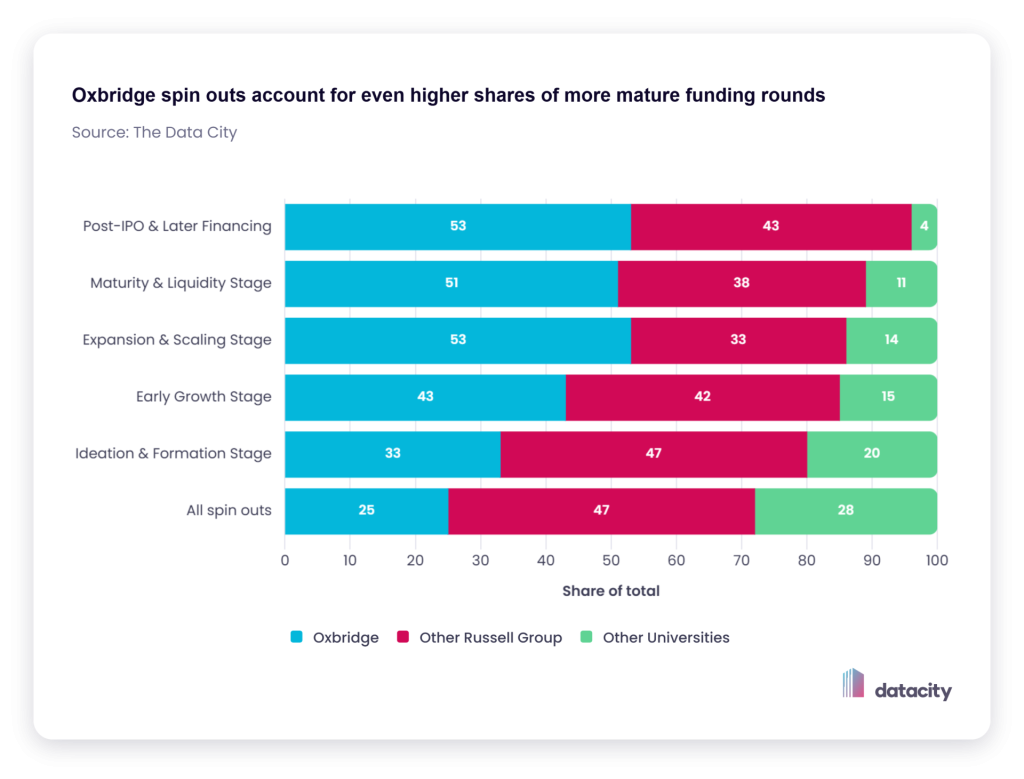

Fact 4: Oxbridge dominates spin out creation and spin out investment even more so

These two universities (led by Cambridge) account for 25% of all spin outs, 37% of all their investment rounds and 59% of all declared investment amounts they have received (see Figure 3).

Their dominance is even more pronounced in some areas. They account for 36% (104/290) of all UK Life Sciences spin outs, 40% (21/53) of semiconductor spin outs and 42% (51/121) of all AI spin outs.

Spin outs from Russell Group universities account for a slightly smaller share of investment rounds than businesses, and smaller shares of volume of investment still. This reflects the smaller likelihood that spin outs from these universities reach later stages of funding (see Figure 4).

The universities that don’t fall into either of these two categories account for a smaller share of spin outs and a smaller share of investment rounds and volume of funding.

Fact 5: University of Swansea is a surprise package

At 44 spin outs, it ranks 8th of any UK university (see Figure 5). But unlike Oxbridge, its spin outs haven’t attracted anywhere near as much investment. On average, Swansea’s spin outs have had 0.7 investment rounds per spin out, compared to 3.0 for those from Cambridge. And most haven’t been beyond the ideas stage – just 12% (4) of the investment rounds in these companies have been beyond ‘Ideation & Formation Stage’, whereas 40% (256) of investment rounds in Cambridge spin outs have been beyond this stage.

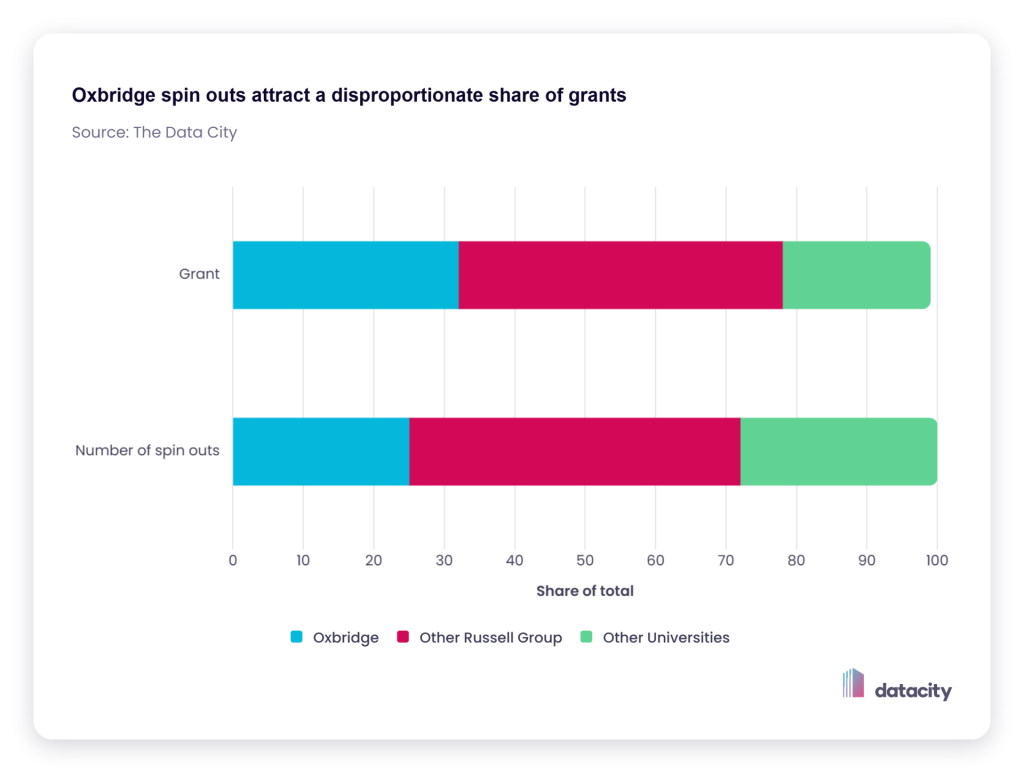

Fact 6: Many spin outs receive grant funding

Despite their perceived high growth potential, many companies do receive public sector support. In addition to support they receive to spin out in the first place from the university, 31% of spin outs trading today have received at least one early-stage grant from a public body. This compares to less than 2% for the wider cohort of companies.

Grant bodies disproportionately award their grants to Oxbridge spin outs, which account for one third of all grants awarded. Russell Group spin outs also receive slightly more grants than the total number of spin outs they account for (see Figure 6). We make no judgment as to whether this is a ‘good’ or a ‘bad’ thing.

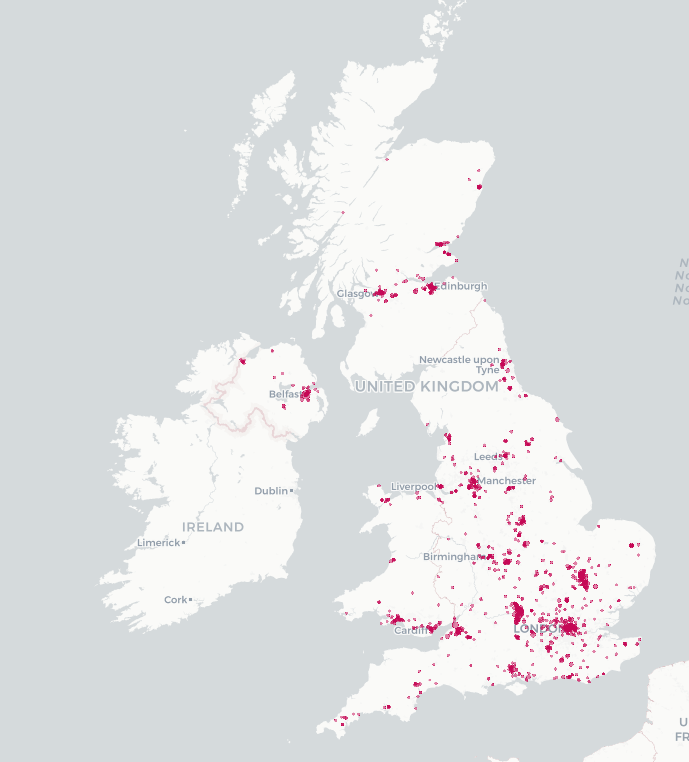

Fact 7: Spin outs are very much urban

Spin outs have a strong preference for an urban location. Figure 7 shows the spread of these companies across the country. While the UK’s 63 largest areas account for 9% of land and 56% of all businesses, they are home to 72% of UK spin outs. Almost a quarter are based in London, while (reflecting the high number of spinouts form their institutions) Cambridge and Oxford follow with around 5% of the total each. Manchester comes 4th (5%), and Edinburgh 5th (3.4%).

What role should spin outs play in the economy?

The data above tells us that university spin outs make up a very small part of the UK business base. But many of them are at the very cutting edge of the economy, shown both by the activities they are involved in and the sums of investment they receive. This helps explain why they receive so much policy attention.

The question is whether policy can increase the number of spin outs so that they have a bigger impact on the economy. Without good international comparisons (which we hope to address) this is a hard question to answer. Two things are clear though. The first is that whatever the best version of UK spin out production looks like, realistically it isn’t going to be an order of magnitude higher than what it is currently. And the second is the value of real time data to inform what approach public policy should take.

Want to know more? Sign in to your Data City account, or sign up for a free trial. Or book a demo of our new University Industry Impact Explorer tool to look at spin outs and other impacts that universities have on the economy.